Payments Architecture Patterns for Regulated Environments

Modern payment systems must deliver speed, scale, and availability—while operating under stringent regulatory, risk, and resilience requirements.

For banks and regulated financial institutions, payments architecture is not just a technology decision; it is a control framework that underpins liquidity, fraud, compliance, and operational stability.

Understanding common architecture patterns—and the trade-offs they introduce—is essential for institutions modernising payments in real-time, ISO 20022–driven environments.

Why Payments Architecture Matters More in Regulated Environments

In regulated institutions, payments platforms must simultaneously support:

- High transaction volumes and 24x7 availability

- Real-time settlement and irrevocability

- Strong fraud, AML, and sanctions controls

- Liquidity and settlement risk management

- Auditability, explainability, and regulatory oversight

Unlike consumer tech platforms, failure modes in payments architectures have regulatory, financial, and reputational consequences.

Core Payments Architecture Patterns

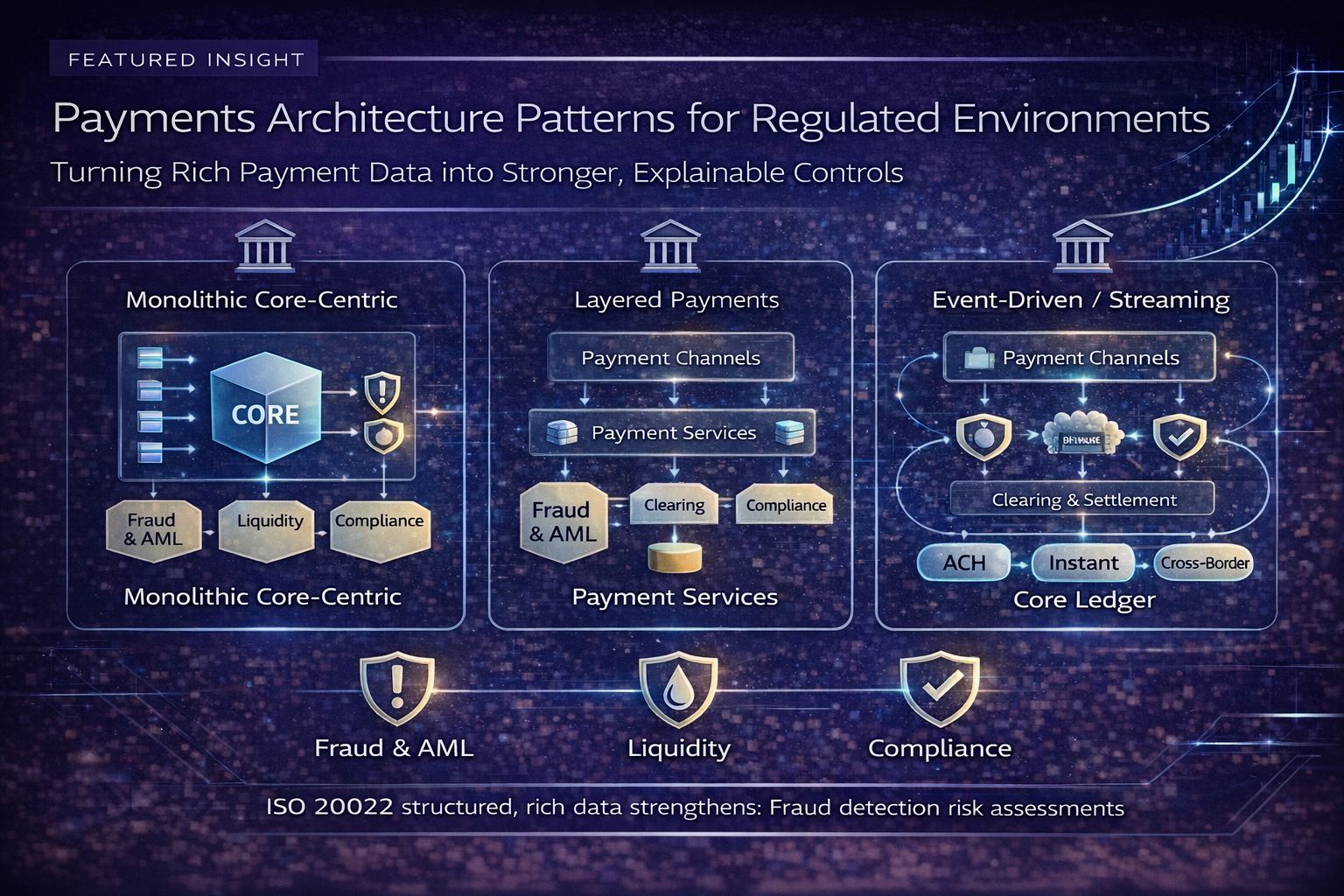

1. Monolithic Core-Centric Architecture

Description

Payments logic is embedded directly within the core banking or ledger system.

Strengths

- Strong data consistency

- Simpler reconciliation

- Clear control ownership

Limitations

- Poor scalability for real-time payments

- Slow change cycles

- High operational risk during upgrades

Regulatory Implication

Often struggles to meet availability and resilience expectations for instant payment rails.

2. Layered Payments Architecture

Description

Payments processing is separated into distinct layers:

- Channel & initiation layer

- Payment orchestration layer

- Clearing & settlement integration

- Risk, fraud, and compliance services

- Core ledger posting

Strengths

- Clear separation of concerns

- Easier regulatory control mapping

- Scalable and resilient

- Supports ISO 20022 coexistence

Risks

- Requires strong orchestration and governance

- Integration complexity if poorly designed

Why Regulators Prefer It

Controls are explicit, testable, and independently scalable.

3. Event-Driven / Streaming Architecture

Description

Payments are processed through asynchronous events using messaging or streaming platforms.

Strengths

- High throughput and resilience

- Natural fit for real-time payments

- Better failure isolation

Challenges

- Harder explainability if poorly governed

- Requires mature monitoring and replay controls

Regulatory Consideration

Must demonstrate determinism, traceability, and controlled recovery paths.

4. Hub-and-Spoke / Payment Orchestration Model

Description

A central payments hub routes transactions to multiple rails (ACH, instant, cross-border).

Strengths

- Single control point for routing and risk

- Simplified scheme integration

- Consistent customer experience

Risks

- Hub becomes a critical dependency

- Requires strong resilience and capacity planning

Regulatory Focus

Concentration risk and recovery capability.

Where Risk and Compliance Must Sit in the Architecture

In regulated environments, risk controls cannot be bolted on.

Effective architectures embed:

- Fraud and APP controls before authorisation

- Liquidity and balance checks inline with execution

- AML and sanctions screening with real-time escalation

- Clear decision points with auditable outcomes

Post-transaction controls alone are no longer sufficient.

ISO 20022 as an Architectural Driver

ISO 20022 materially influences architecture design by:

- Increasing data volume and structure

- Enabling richer fraud and AML signals

- Raising expectations for explainability

- Supporting coexistence and phased migration

Architectures must be designed to use ISO 20022 data, not merely transport it.

Common Failure Patterns

Institutions often encounter problems when they:

- Over-centralise logic in the core

- Treat real-time payments as “just another rail”

- Rely on batch-based fraud and AML controls

- Underestimate liquidity and settlement dependencies

- Design for throughput but not recoverability

These issues typically surface during stress events, not normal operations.

Designing for Resilience and Supervision

Leading institutions design payments architectures that:

- Fail safely and predictably

- Support partial degradation rather than total outage

- Enable real-time monitoring and intervention

- Provide clear evidence for regulators and auditors

- Align technology boundaries with operational ownership

Architecture and operating model must evolve together.

Key Takeaway

In regulated environments, payments architecture is risk architecture.

Institutions that adopt layered, well-governed, and data-rich architecture patterns are far better positioned to:

- Scale real-time payments safely

- Meet ISO 20022 and supervisory expectations

- Control fraud, liquidity, and operational risk

- Modernise without destabilising core systems

The right architecture does not just process payments—it protects the institution.