Using ISO 20022 Data for Fraud and AML Effectiveness

Turning Rich Payment Data into Stronger, Explainable Controls

ISO 20022 is transforming payments by introducing structured, standardised, and semantically rich data. Yet many institutions stop at technical compliance—failing to unlock the real value of ISO 20022 in fraud prevention and AML effectiveness.

In a world of real-time, irreversible payments and rising regulatory scrutiny, how ISO 20022 data is used matters as much as whether it is present. Institutions that redesign fraud and AML controls around ISO 20022 gain stronger detection, lower false positives, and far greater explainability.

Why ISO 20022 Changes Fraud and AML Outcomes

Traditional payment formats relied heavily on:

- Free-text fields

- Inconsistent population of key attributes

- Limited counterparty and transaction context

ISO 20022 fundamentally changes this by providing:

- Structured party and account identification

- Clear debtor, creditor, and agent roles

- Purpose codes and rich remittance information

- End-to-end transaction identifiers

This richness enables better signal quality, not just more data.

From Data Presence to Data Use

Many institutions fall into a common trap:

- ISO 20022 messages are received

- Data is flattened or truncated

- Legacy fraud and AML rules remain unchanged

In these cases, detection quality does not materially improve, and regulatory value is lost.

True effectiveness comes when fraud and AML frameworks are redesigned to consume ISO 20022 data natively.

How ISO 20022 Improves Fraud Detection

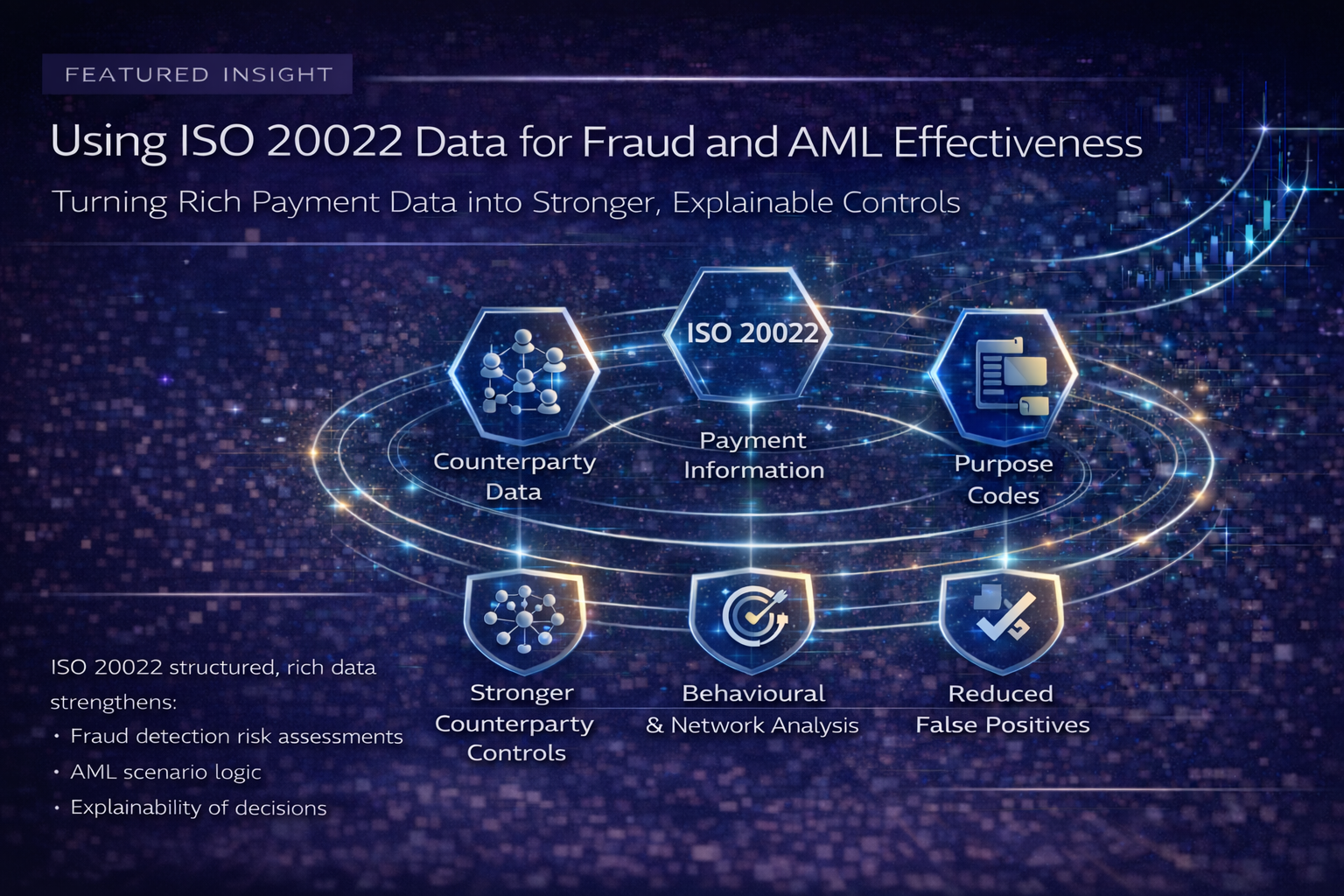

Stronger Counterparty Risk Assessment

Structured party data enables:

- Clear identification of first-time or high-risk payees

- Better beneficiary reputation analysis

- Improved detection of mule accounts and networks

Payee clarity is critical for APP fraud and scam prevention.

Better Behavioural and Contextual Analysis

ISO 20022 supports:

- Clear transaction intent via purpose codes

- Richer context for behavioural deviation analysis

- Differentiation between normal and suspicious activity

This reduces reliance on blunt amount-based thresholds.

Reduced False Positives

With better context:

- Legitimate transactions are less likely to be flagged

- Alerts are more meaningful

- Investigator time is focused on genuine risk

Improved data quality directly improves operational efficiency.

Strengthening AML and Transaction Monitoring with ISO 20022

Clearer Scenarios and Typologies

ISO 20022 enables:

- More precise customer and counterparty segmentation

- Stronger typology-driven scenarios

- Better identification of structuring, smurfing, and mule behaviour

Scenarios become behaviour-based, not purely transactional.

Improved SAR Quality and Defensibility

Structured data supports:

- Clearer narratives

- Stronger linkage between transactions

- Better evidence of suspicious intent

This improves both regulatory confidence and investigation quality.

Network and Relationship Analysis

ISO 20022 enhances:

- Flow-of-funds analysis

- Network connectivity detection

- Identification of coordinated activity across accounts

These capabilities are critical in real-time environments where value disperses quickly.

Explainability: A Regulatory Imperative

Regulators increasingly ask:

- Why was this transaction flagged—or allowed?

- Which data influenced the decision?

- Was the logic applied consistently?

ISO 20022 supports explainability by:

- Linking decisions to specific, structured data elements

- Improving traceability across systems

- Enabling reproducible outcomes during audits

Explainability must be designed into controls, not reconstructed later.

Design Principles for Using ISO 20022 Effectively

Leading institutions follow five principles:

- ISO 20022 as the canonical data model

Legacy formats are translated at the edges only.

- Preserve data richness end-to-end

Avoid truncation and uncontrolled transformation.

- Redesign fraud and AML logic

Rules and models must consume structured fields directly.

- Integrate fraud and AML signals

Use shared data foundations to detect end-to-end activity.

- Embed governance and lineage

Ownership, quality controls, and explainability are mandatory.

Common Pitfalls to Avoid

Institutions often undermine value when they:

- Treat ISO 20022 as a transport upgrade

- Apply legacy rules unchanged

- Lose data during coexistence

- Fail to align fraud, AML, and reporting systems

- Cannot explain automated decisions

These gaps are a growing source of regulatory findings.

Key Takeaway

ISO 20022 does not improve fraud and AML outcomes by default—design does.

Institutions that:

- Use ISO 20022 as a canonical data foundation

- Redesign fraud and AML controls around structured data

- Preserve explainability and lineage

- Integrate fraud and financial crime intelligence

can significantly improve detection effectiveness, reduce false positives, and meet rising regulatory expectations—while supporting real-time payments and digital growth.